In the previous section, tax accountant Gohei Fujimoto explained the current situation and issues of the cryptocurrency tax system, as well as future revisions, but from here on, we will explain it with specific examples. Before that, we will explain the basic premise of the current cryptocurrency tax system again.

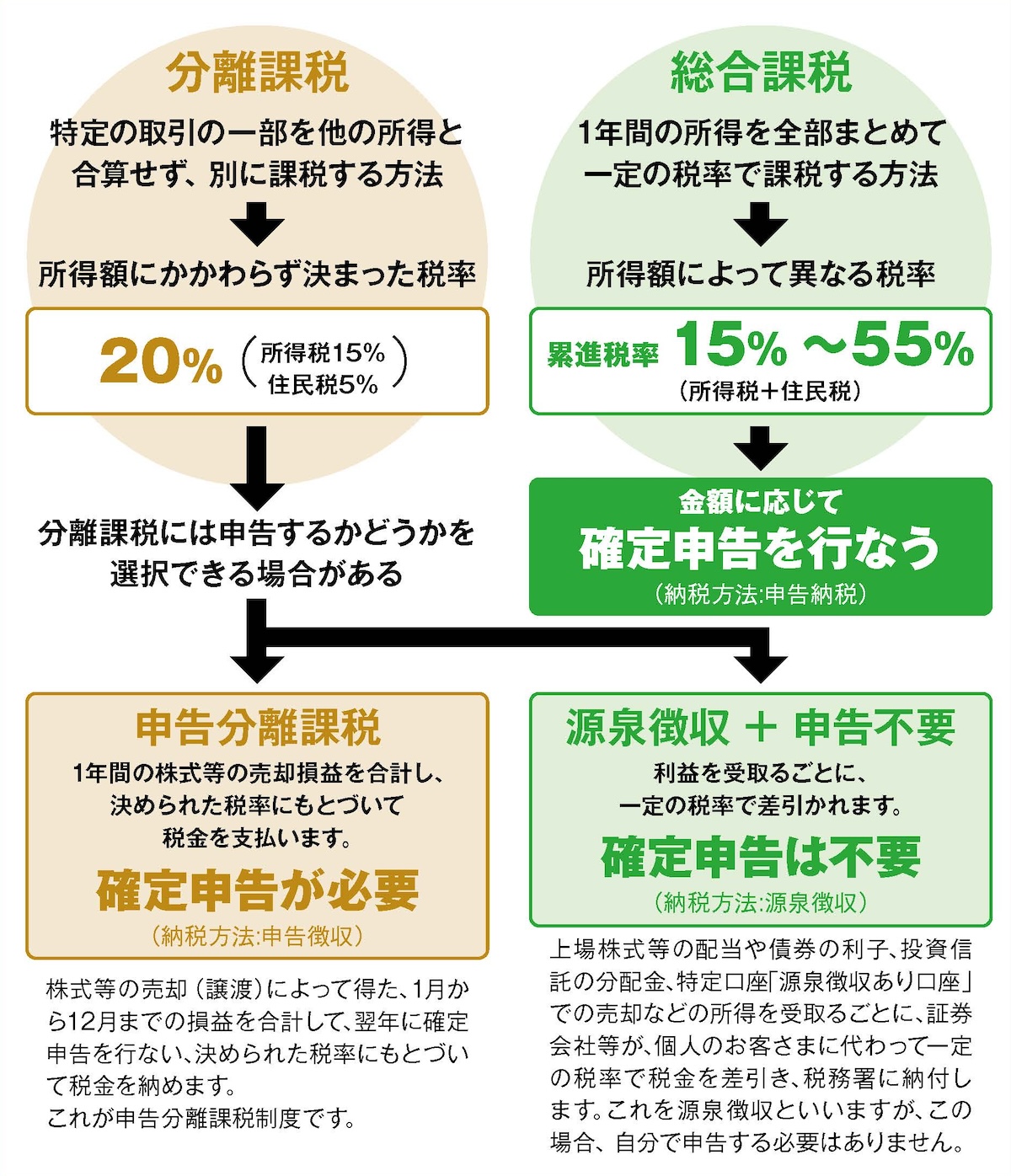

First, profits earned by individuals from buying and selling cryptocurrencies and mining are treated as "miscellaneous income" out of the 10 types of income classification. Miscellaneous income is subject to comprehensive taxation, and the tax rate is determined by the amount combined with other income such as salary income and real estate income.

It is a common misconception that 55% of profits generated from cryptocurrencies are not subject to taxation. In addition, the figure of 55% is the sum of the maximum income tax rate of 45% in the excess progressive tax rate and the resident tax of 10%. The income amount at which the tax rate changes is posted on the National Tax Agency's website, so please check the latest information from time to time.

In addition, if the income of miscellaneous income exceeds 200,000 yen after deducting expenses, etc., a tax return is required. Therefore, for example, if you buy Bitcoin for 1 million yen per BTC and sell it for 1.2 million yen, the difference of 200,000 yen will be taxable and you will need to file a tax return.

This is just a simple pattern, and in reality, you will make several, dozens, or even hundreds of transactions, so in order to accurately understand, you should record and store your transaction history carefully. In addition, individuals are not subject to taxation on unrealized gains from crypto assets.

Even if you buy Bitcoin for 1 million yen per BTC and the price rises to 1.3 million yen, you will not be taxed as long as you do not sell it. Furthermore, if you have losses from other crypto asset transactions and do not make a profit of more than 200,000 yen when you add up your profits and losses, you will not need to file a tax return.

For example, suppose you made a profit of 300,000 yen from trading Bitcoin, but lost 150,000 yen from buying and selling Ethereum. In that case, the difference is 150,000 yen, so you are not required to file a tax return.

These are just the basics of crypto asset taxes. From here on, we will summarize the current discussions taking into account this situation.

Point 1. Profits from cryptocurrencies are miscellaneous income, and we expect the application of separate reporting taxation in the future.

▶Excerpt from Daiwa Securities' "Basic knowledge of tax (1)" and created by the editorial department

Crypto assets to be subject to separate taxation and loss carryover deduction

The current cryptocurrency tax system is a major obstacle to the spread of Web 3.0. Therefore, industry groups such as JVCEA (Japan Cryptocurrency Exchange Association) and JCBA (Japan Cryptocurrency Business Association) are calling for the application of 20% separate taxation and three-year loss carryover deduction for profits generated from crypto assets.

If crypto assets are subject to separate taxation, they can be reported separately from other income, and the tax rate will be a flat 20%. Therefore, it is expected that the barrier to exposure to crypto assets will be lowered more than ever before, and that this will lead to the revitalization of cryptocurrency trading in Japan. Crypto assets are subject to drastic price fluctuations, and a sudden increase in price can lead to large profits. In such cases, if it is miscellaneous income, you may be hesitant to sell it because you are thinking about the tax you will have to pay, but the application of 20% separate taxation will make it possible to maximize profits.

In addition, the tax burden will be reduced by applying a three-year loss carryover deduction. In particular, crypto assets can bring about large profits, but on the other hand, they can also cause unimaginable losses. In such cases, under the current tax system, even if you incur a large loss in one year and make a large profit the following year, you will still be subject to taxation.

For example, if you incur a loss of 1 million yen in crypto assets in one year, but make a profit of 200,000 yen the following year, the combined income of this 200,000 yen and other income will be subject to taxation. This still does not fully cover the loss of 800,000 yen.

So, what will happen if a three-year loss carryover deduction is applied? Similarly, let's say you incur a loss of 1 million yen in crypto assets in one year, but make a profit of 200,000 yen the following year. Since loss carryover deductions allow losses to be carried forward to the following year, in this case the profits made in the year following the loss are offset, and the taxable amount will be 0 yen.

Such tax system reforms have been requested by the industry for a long time. There are various other requests, but these reforms are the top priority above all else, and if they are realized, they will have a major impact on the industry.

→ "Everyone should be prepared to file tax returns"

The article is for members only. Please sign up to continue reading.

MAGAZINE

Iolite Vol.20

July 2026 issueReleased on 2026/05/29

Interview Michael Shaulov, CEO & Co-Founder of Fireblocks

Marcus Infanger, SVP of RippleX

PHOTO & INTERVIEW Ryoko Yonekura

Special Features

"The Future of Payments: Beyond the Gateway"

"Innovation Without Taboos: The Dual-Use Shockwave"

"The Future of Humanity Expanded by BMI: The 'Sixth Sense' Stemming from Brain-Computer Interface Devices"

[Dialogue Series] The NISHI Talk: Crypto Conversations"The 'True Decentralization' of DeFi and the Challenges Facing the Crypto Industry"

Kasou NISHI × Yoshihiko Uchida

Series Tech and Future by Toshinao Sasaki... and more.

MAGAZINE

Iolite Vol.20

July 2026 issueReleased on 2026/05/29

Interview Michael Shaulov, CEO & Co-Founder of Fireblocks

Marcus Infanger, SVP of RippleX

PHOTO & INTERVIEW Ryoko Yonekura

Special Features

"The Future of Payments: Beyond the Gateway"

"Innovation Without Taboos: The Dual-Use Shockwave"

"The Future of Humanity Expanded by BMI: The 'Sixth Sense' Stemming from Brain-Computer Interface Devices"

[Dialogue Series] The NISHI Talk: Crypto Conversations"The 'True Decentralization' of DeFi and the Challenges Facing the Crypto Industry"

Kasou NISHI × Yoshihiko Uchida

Series Tech and Future by Toshinao Sasaki... and more.