The End of the Boom and the Transition to Public Goods: Legal Reforms and the Current State of Accounting and Auditing | Interview with Keishi Tanaka and Yoshiyuki Kawamura of EY ShinNihon LLC

Vertical Integration of Crypto Asset Exchanges and the Definition of Unfair Trading

Summary

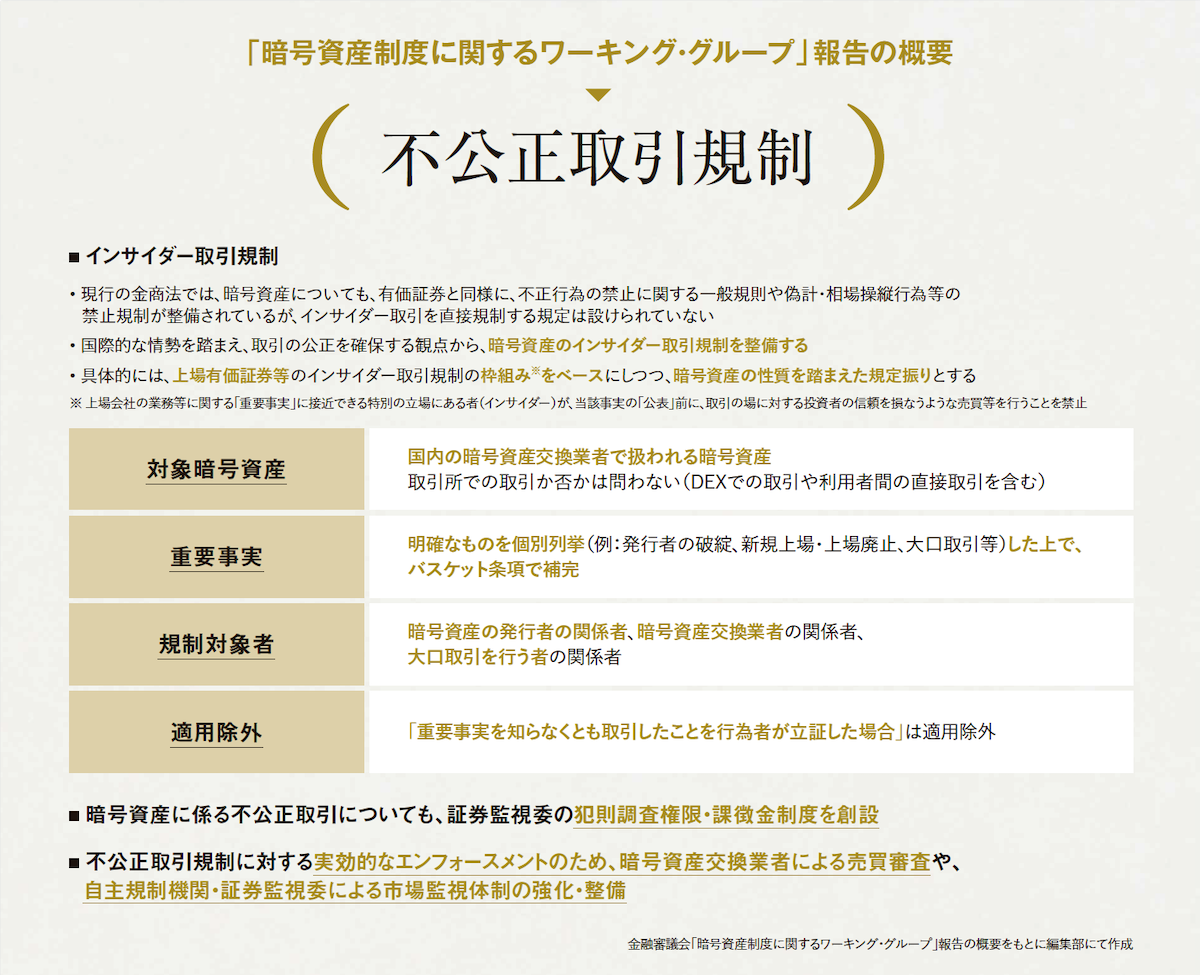

【Information Regulation】Summary of the 'Working Group on Crypto Asset Systems' Report

How do you both perceive the changes surrounding crypto assets?

Tanaka: I have been involved in accounting and auditing in this industry for about 7-8 years. A few years ago, there was a rapid surge in interest around keywords like NFTs and the metaverse, and many people were drawn to the movement to create ecosystems.

During that time, there was a noticeable increase in young accountants expressing interest in Web3.0.

However, I think the enthusiasm has significantly cooled down over the past 1-2 years. The number of startups seeking audits with the aim of pursuing an IPO in Web3.0 business has also markedly decreased compared to 2-3 years ago.

On the other hand, I don't think that interest in Web3.0 itself has waned.

For example, companies adopting treasury strategies, assuming a certain level of financial power, are entering the market. It's not just a temporary boom; companies that continuously engage with changing genres and perspectives are still around.

The so-called 'fleeting excitement' has passed, but serious businesses continue to exist and grow in their respective fields. That's how I see it.

Kawamura: The report of the Financial Services Agency's 'Working Group on Crypto Asset Systems' for the fiscal year 2025, which notes the legal framework transition of crypto assets from the Funds Settlement Act to the Financial Instruments and Exchange Act, indicates that crypto assets are becoming 'public goods.'

Previously, crypto assets were regulated under the Funds Settlement Act, giving the impression that they were somewhat peripheral to financial products.

This transition to a framework similar to that of securities represents a significant shift.

In discussions on tax reform, the country's stance is not to encourage investment in crypto assets, but it is evident that the approach assumes more people will participate for asset formation purposes through NISA and ETFs, including those with high literacy in traditional crypto assets and those participating for speculative reasons.

This implies that it will be necessary to provide a certain level of trust and protection even to those who are not familiar with crypto assets. As an auditing firm, we must be aware of these changes and engage in audits of related companies accordingly.

Compared to traditional financial markets like the stock market, are there risks that make unfair trading 'easier to detect' because it's on-chain?

Kawamura: This point can be difficult to understand without grasping the structure of crypto asset exchanges.

For instance, crypto asset exchanges like bitFlyer and Coincheck effectively combine the functions of both a brokerage firm and a stock exchange.

In stock trading, you first open an account with a brokerage firm, and orders are placed with the Tokyo Stock Exchange. Brokerage firms and exchanges are separate entities. However, crypto asset exchanges provide both functions within a single company. This 'vertical integration' makes monitoring unfair trading challenging.

Each company has its own private market, making the price formation process opaque from the outside.

For example, if you open an account with bitFlyer and buy Bitcoin, that transaction is completed within bitFlyer's market. The same goes for Coincheck. Each exchange operates its own independent market. This structure is not well understood by the general public.

Moreover, compared to markets like the Tokyo Stock Exchange, which have ample liquidity and strict regulations, the markets of various crypto asset exchanges vary in size and regulatory intensity.

From the perspective of market manipulation as a form of unfair trading, it's essential to note that most crypto asset transactions are not conducted on-chain.

For instance, when a user buys Bitcoin, the transaction history is not directly recorded on the blockchain. Instead, the exchange's internal system merely adjusts the balances between customers.

Thus, most unfair trading occurs not on-chain but within the somewhat closed world of the exchange's internal systems. Therefore, it's necessary to assess unfair trading on a market-by-market basis within each exchange.

This aspect cannot be captured by on-chain analysis alone. It's a challenge for the Securities and Exchange Surveillance Commission to see how far it can view the internal transaction data of all the more than 20 crypto asset exchanges in the country.

This issue is not unique to Japan. Exchanges worldwide, including Coinbase and Binance, also combine the functions of a market and a brokerage firm. As a result, even for a single Bitcoin, there are thousands of markets worldwide, each with different prices. Unlike the stock market, where price differences narrow due to liquidity, this structure is different.

In traditional securities markets, market manipulation is assessed based on order book trading, but the crypto asset market operates 24/7, and the concept of order book does not exist.

In this structure, it's not possible to directly apply rules based on order books and indicative prices, as in the stock market. Each operator has different systems and operations. Therefore, the criteria for defining market manipulation are still not well organized.

As a result, it's challenging to define and regulate unfair trading in the same way as in traditional securities markets.

The article is for members only. Please sign up to continue reading.

MAGAZINE

Iolite Vol.21

September 2026 issueReleased on 2026/07/30

Interview Richard Teng, Co-CEO, Binance

Taisuke Isono, Head of Nikko Open Innovation Lab & DeFi Technology Department, SMBC Nikko Securities Inc.

Hiroshi Kamiwaki, Director & Head of Crypto Asset Finance Business, Fintertech Co., Ltd.

PHOTO & INTERVIEW Yusaku Nakano

Feature Story: "Survival Strategies for Crypto Exchanges — The New Order Post-FIEA Transition"

Interview

Tomoyuki Isaka, President & Representative Director, CEO, Coincheck, Inc.

Takaaki Fujiwara, Executive Vice President & Director, Mercury Inc.

[Dialogue Series] The NISHI Talk: Crypto Conversations

"Social Implementation Beyond Merely Holding Bitcoin"

Kasou NISHI × Rintaro Kawai, President & Representative Director, ANAP HOLDINGS Co., Ltd.

Series: Tech and Future Toshinao Sasaki ...and more

MAGAZINE

Iolite Vol.21

September 2026 issueReleased on 2026/07/30

Interview Richard Teng, Co-CEO, Binance

Taisuke Isono, Head of Nikko Open Innovation Lab & DeFi Technology Department, SMBC Nikko Securities Inc.

Hiroshi Kamiwaki, Director & Head of Crypto Asset Finance Business, Fintertech Co., Ltd.

PHOTO & INTERVIEW Yusaku Nakano

Feature Story: "Survival Strategies for Crypto Exchanges — The New Order Post-FIEA Transition"

Interview

Tomoyuki Isaka, President & Representative Director, CEO, Coincheck, Inc.

Takaaki Fujiwara, Executive Vice President & Director, Mercury Inc.

[Dialogue Series] The NISHI Talk: Crypto Conversations

"Social Implementation Beyond Merely Holding Bitcoin"

Kasou NISHI × Rintaro Kawai, President & Representative Director, ANAP HOLDINGS Co., Ltd.

Series: Tech and Future Toshinao Sasaki ...and more