What are the challenges facing the newly formed five major economic zones?

As we enter 2024, I think there have been major changes in what have been called the four major economic zones. Could you first give us a brief overview of those trends?

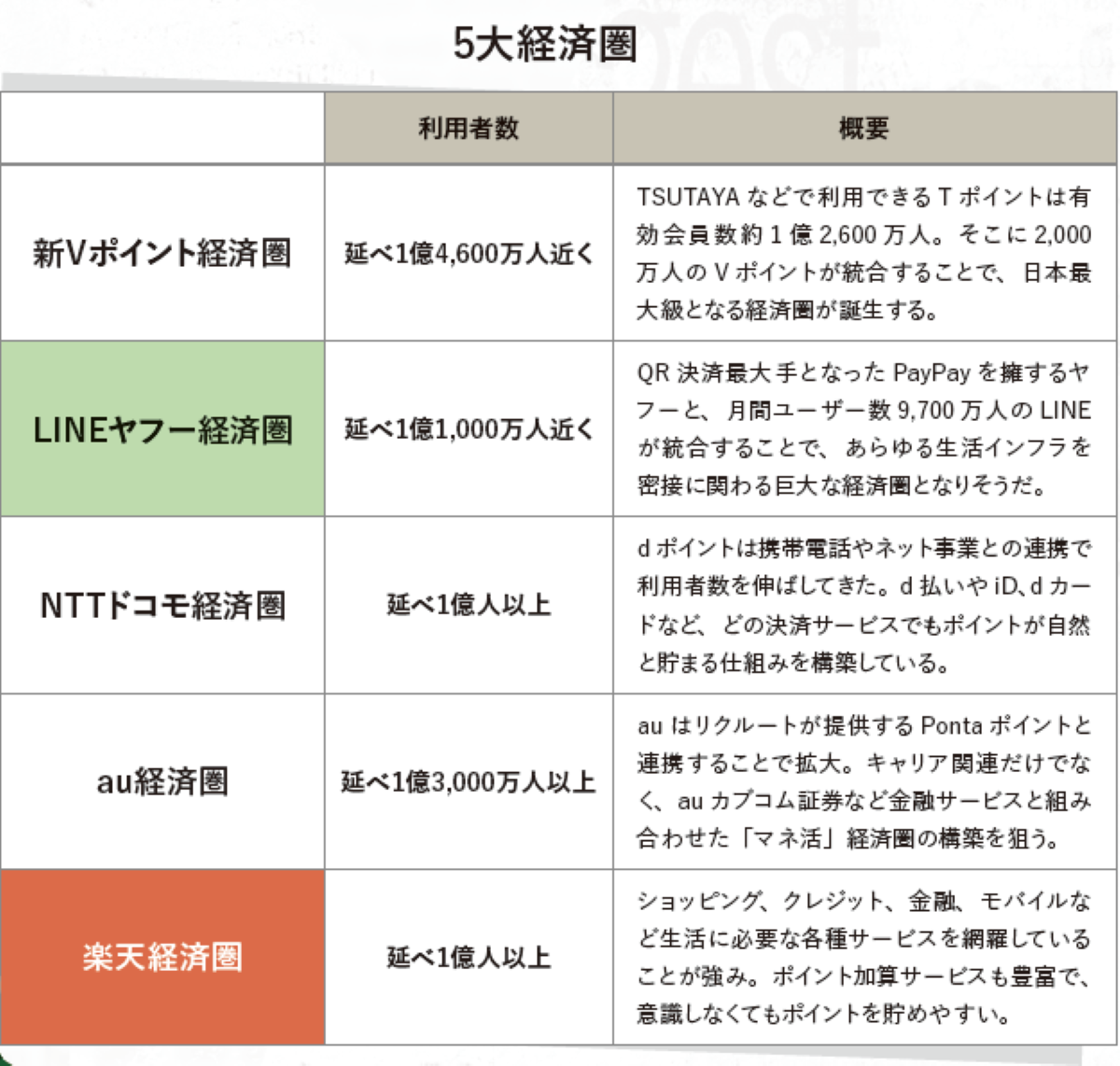

Arai: As we enter 2024, what were previously called the four major economic zones have been merged with T-Point and V-Point to form a new economic zone called the five major economic zones, called the "New V-Point." It is said that the New V-Point economic zone will threaten the Rakuten economic zone, which has had a particularly stronghold among the economic zones.

Among them, the LINE economy was a hot topic last year when it was said to be merging with Yahoo to form a new economic sphere. Could you tell us about its origins?

Arai: The origins of each economy are roughly the same. The LINE economy has LINE, and the Rakuten economy has Rakuten Ichiba, and they have platforms as factors that form the economy. Having a platform means having personal IDs and purchasing data. Here too, there are factors that form the economy. The mechanism that forms the economy is that the action steps from when a customer recognizes a product to when they purchase it, that is, the services in each funnel, can be completed within the same platform.

In the case of LINE, an economic sphere is formed when LINE users who see a LINE ad shop with LINE Pay, and then participate in campaigns and earn LINE points by using the LINE credit card, creating a flow. The LINE economy has a lineup of services that rivals Rakuten, including LINE Shopping, LINE Securities, LINE Pocket Money, LINE Smart Investment, LINE Coupons, and LINE FX, and these services can be accessed from the "wallet" on LINE.

The article is for members only. Please sign up to continue reading.

MAGAZINE

Iolite Vol.21

September 2026 issueReleased on 2026/07/30

Interview Richard Teng, Co-CEO, Binance

Taisuke Isono, Head of Nikko Open Innovation Lab & DeFi Technology Department, SMBC Nikko Securities Inc.

Hiroshi Kamiwaki, Director & Head of Crypto Asset Finance Business, Fintertech Co., Ltd.

PHOTO & INTERVIEW Yusaku Nakano

Feature Story: "Survival Strategies for Crypto Exchanges — The New Order Post-FIEA Transition"

Interview

Tomoyuki Isaka, President & Representative Director, CEO, Coincheck, Inc.

Takaaki Fujiwara, Executive Vice President & Director, Mercury Inc.

[Dialogue Series] The NISHI Talk: Crypto Conversations

"Social Implementation Beyond Merely Holding Bitcoin"

Kasou NISHI × Rintaro Kawai, President & Representative Director, ANAP HOLDINGS Co., Ltd.

Series: Tech and Future Toshinao Sasaki ...and more

MAGAZINE

Iolite Vol.21

September 2026 issueReleased on 2026/07/30

Interview Richard Teng, Co-CEO, Binance

Taisuke Isono, Head of Nikko Open Innovation Lab & DeFi Technology Department, SMBC Nikko Securities Inc.

Hiroshi Kamiwaki, Director & Head of Crypto Asset Finance Business, Fintertech Co., Ltd.

PHOTO & INTERVIEW Yusaku Nakano

Feature Story: "Survival Strategies for Crypto Exchanges — The New Order Post-FIEA Transition"

Interview

Tomoyuki Isaka, President & Representative Director, CEO, Coincheck, Inc.

Takaaki Fujiwara, Executive Vice President & Director, Mercury Inc.

[Dialogue Series] The NISHI Talk: Crypto Conversations

"Social Implementation Beyond Merely Holding Bitcoin"

Kasou NISHI × Rintaro Kawai, President & Representative Director, ANAP HOLDINGS Co., Ltd.

Series: Tech and Future Toshinao Sasaki ...and more