個人が暗号資産の売買やマイニングで得た利益は、10種類ある所得区分のうち「雑所得」として扱われる。雑所得は総合課税の対象となり、給与所得や不動産所得など、ほかの所得とあわせた額によって税率が決まる。

よくある誤解だが、暗号資産によって生じた利益のうち55%相当が課税対象となるわけではない。また、55%という数字は超過累進税率における最大の所得税率45%と、住民税10%を合算した数字だ。税率が変わる所得金額は国税庁のホームページにて掲載されているため、最新の情報を都度確認していただきたい。

なお、雑所得は経費などを差し引いた所得が20万円を超えると確定申告を行う必要がある。そのため、たとえばビットコインを1BTCあたり100万円で購入し、120万円で売却した場合、差額の20万円は課税対象となり確定申告を行う必要が生じる。

これはあくまでもシンプルなパターンであり、実際には数回、数十回、または数百回以上の取引を行うことになるため、正確に把握するためにはこまめに取引履歴を記録・保管しておくべきだろう。また、個人については暗号資産による含み益は課税対象とならない。

仮にビットコインを1BTCあたり100万円で購入し、価格が130万円まで上がっていたとしても、売却さえしなければ課税対象とはならない。さらに、暗号資産のほかの取引で損失が出ており、損益を合算した際に20万円以上の利益が発生していないケースも確定申告の必要はなくなる。

例として、ビットコインの取引で30万円の利益が出たけれども、イーサリアムの売買によって15万円の損失が発生したとする。その場合は差額が15万円となるため、申告義務は生じない。

これらはあくまでも暗号資産に関する税金の基本となる。ここからはこうした状況を踏まえて現在議論されている内容を整理していく。

Point 1.暗号資産で得た利益は雑所得今後は申告分離課税の適用に期待

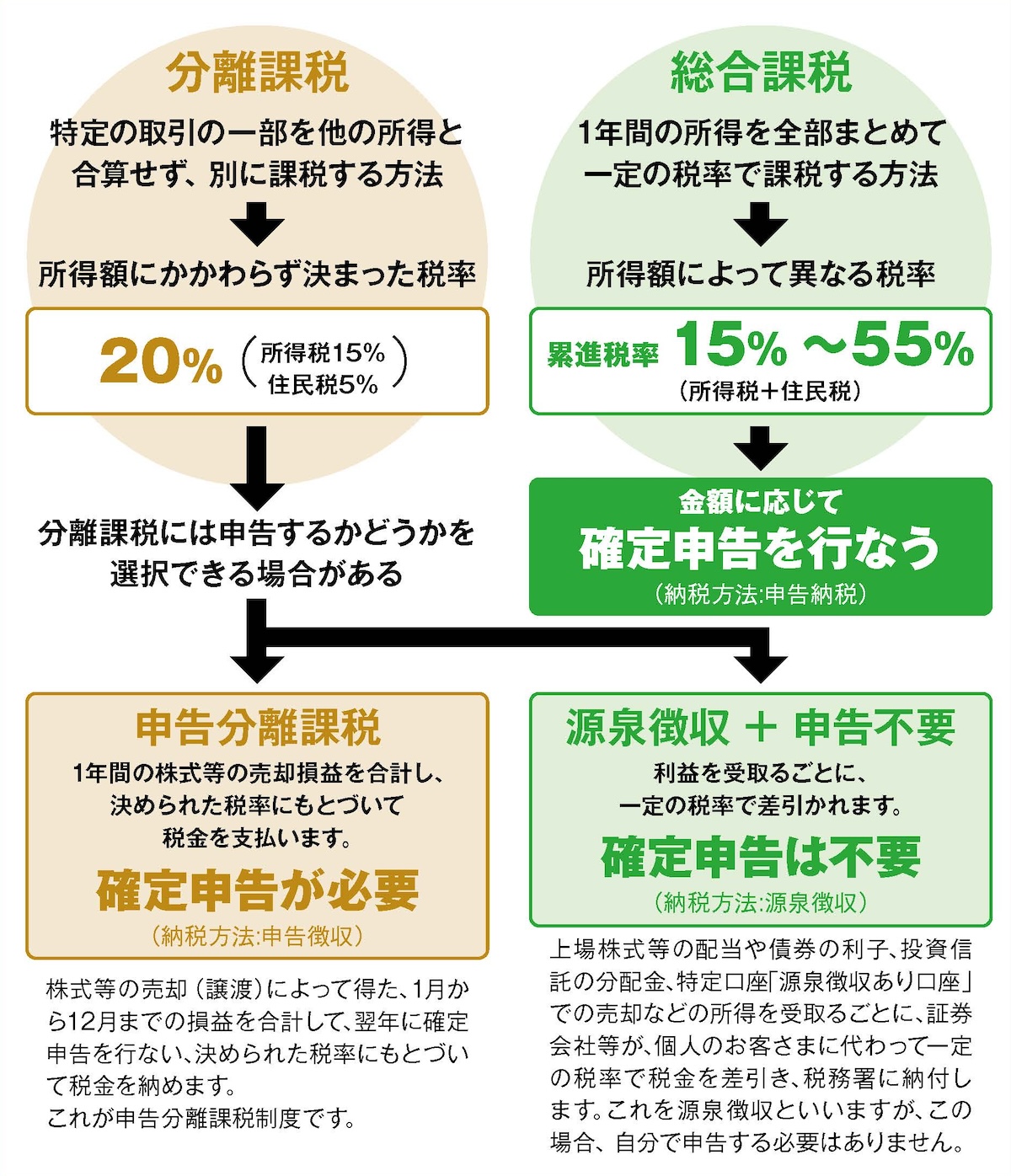

▶大和証券「税金の基礎知識(1)」より内容を抜粋し編集部にて作成

▶大和証券「税金の基礎知識(1)」より内容を抜粋し編集部にて作成暗号資産を申告分離課税と損失繰越控除の対象に

現在の暗号資産税制はWeb3.0の普及に向けた大きな足かせとなっている。そこでJVCEA(日本暗号資産取引業協会)やJCBA(日本暗号資産ビジネス協会)などの業界団体は、暗号資産で生じた利益に対して20%の申告分離課税と3年間の損失繰越控除の適用を求めている。

申告分離課税の対象とすると、ほかの所得とは分離して申告を行うことができ、税率も一律20%となる。そのため、これまで以上に暗号資産に触れるハードルがさがり、国内における暗号資産取引の活性化にもつながることが期待されている。暗号資産は価格変動が激しく、急な値上がりにより大きな利益を得られることがある。その際、雑所得であれば支払う税金のことを考えてしまい売却に迷いが生じる可能性もあるが、20%の申告分離課税が適用されることで利益を最大化することが可能となる。

また、3年間の損失繰越控除を適用することで税負担が軽減される。特に暗号資産は大きな利益を得られる可能性もあれば、逆に目もあてられない損失を被ることもある。その際、現行の税制では仮にその年に大きな損失を生み、翌年に大きな利益を出したとしても課税対象となってしまう。

たとえば、ある年に暗号資産で100万円の損失が生じたものの、翌年に20万円の利益が発生した場合、この20万円とほかの所得を合算した所得が課税対象となる。これではまだ80万円の損失が埋めきれていない。

では、3年間の損失繰越控除を適用した場合にはどうなるだろうか。同じようにある年に暗号資産で100万円の損失が生じたものの、翌年に20万円の利益が発生したとしよう。損失繰越控除は損失を翌年以降に繰り越せることから、このケースでは損失を生んだ翌年に発生した利益が相殺され、課税対象額は0円となる。

こうした税制の改正は、長きにわたって業界から要望されている。このほかにもさまざまな要望が出されているが、何よりもこれらの改正が最優先事項となっており、実現した際には業界に大きなインパクトを与えることになる。

→”誰しもが確定申告をする心構えを持っておこう”