On October 10th, a malfunction occurred in the Zengin Net (National Bank Fund Settlement Network), a system that handles the transfer of funds between financial institutions, causing delays in transfers at some financial institutions and affecting approximately 5 million transactions.

The fact that the system malfunction occurred on the day of the "Gotoubi (50th day of the month)", which is said to be a large number of commercial transactions, is also said to be one of the factors that affected many transactions. It was confirmed that the system was operating normally by the morning of the 12th, and it seems to have been restored.

◉ "Editor-in-Chief Focus" The editor-in-chief of "Iolite", a business magazine that covers next-generation technology and finance/economic topics, follows the hot topics and the forefront of current topics.

Chief Cabinet Secretary Matsuno said at a press conference, "According to the report to the Financial Services Agency, the cause of this failure is unlikely to be a cyber attack, and is thought to be a malfunction that occurred during the update of the system connecting the 'Zengin System' and financial institutions last weekend."

The exact cause is still unknown at this time, but as Chief Cabinet Secretary Matsuno also stated at the press conference, there is said to have been a problem with a specific program in the Zengin Net's relay computer during the process of updating to new software during the three-day holiday from October 7th to 9th.

This is because the failure did not occur at three of the 14 banks that calculated fees using their own systems, but the malfunction occurred at the remaining 11 banks that calculated the domestic foreign exchange system operating expenses on the relay computer side.

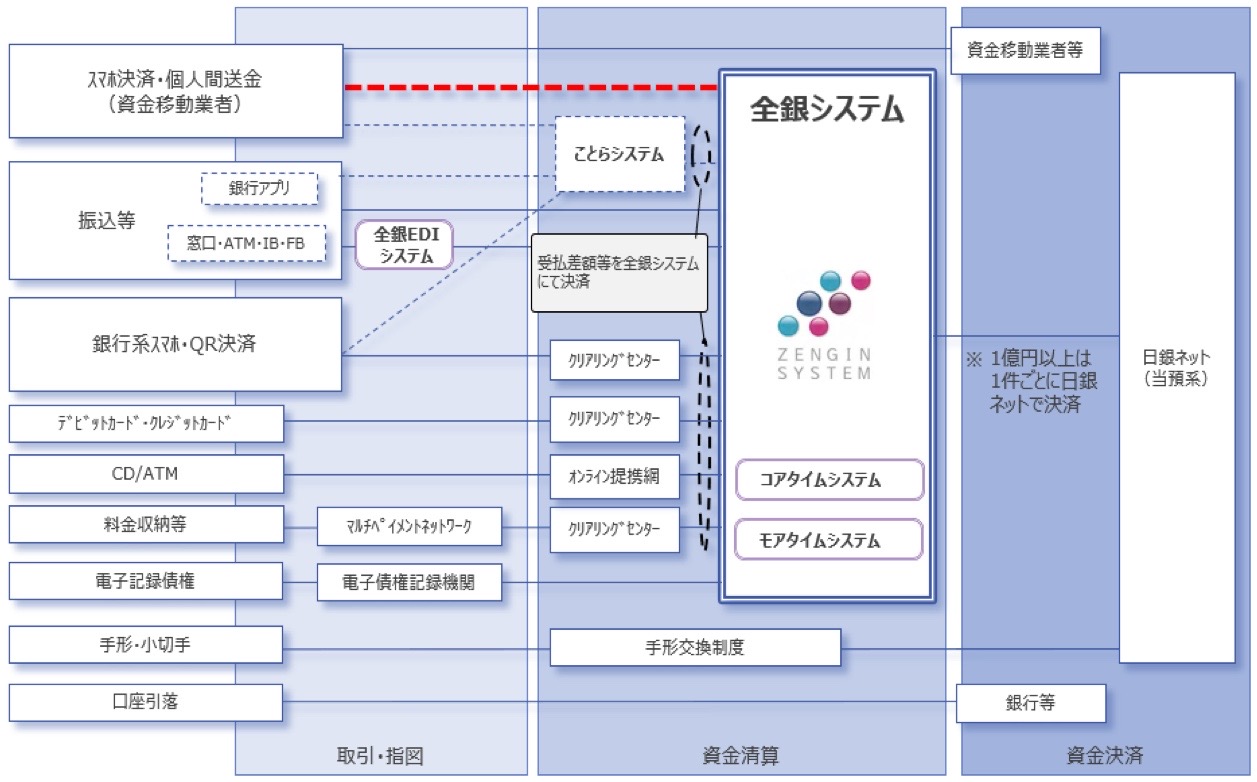

Zengin Net has not experienced any noticeable malfunctions that affected general users in the approximately 50 years since its launch in 1973, and has processed around 14 trillion yen of transactions per day.

Problems that could have actually occurred due to the Zengin-Net system failure

I feel that the fact that they have been able to complete huge, massive transactions without any noticeable problems for approximately 50 years is a trustworthy track record, but I would like to consider some possible cases where a problem may arise when a transfer cannot be made.

Late fee incurred when a transfer cannot be made due to financial debt

Opportunity loss due to failure to complete a profitable transaction

Damage caused by delayed processing that limits losses

Some examples would be:

If you owe money and are unable to make a transfer, you may be charged a late fee

Delays in remittances can cause very serious problems when pursuing financial debts. Under the Civil Code, even if you have completed the transfer request to the bank designated by the creditor, if the transfer result is not reflected on the due date, it is not considered to have been fulfilled (Civil Code Article 477).

To be precise, it may be better to say that there is room for exemption, but it is limited.

Opportunity losses such as failure to conclude profitable transactions

If a transaction occurs in which a payment made after the deadline is not accepted for purchase or application, you will not be able to receive the benefits that you would have been able to enjoy in the future. You may even have to give up a product that you have obtained through a lottery after much effort.

Damages due to delays in processing that can limit losses

If investors are unable to add funds to make up for margin shortfalls in securities and foreign exchange transactions, they are at a higher risk of being forced to make margin calls.

In fact, on Wednesday, October 11, the day after the three-day weekend, the US Producer Price Index (PPI Core Index) for September was released, along with the minutes of the Federal Open Market Committee (FOMC), which may have left some investors scratching their heads.

Fair Trade Commission's efforts to improve the environment: promoting innovation and improving user convenience

The purpose of the Japan Fair Trade Commission's survey was to revitalize financial services that have traditionally been provided mainly by banks and other financial institutions with the entry of businesses that utilize fintech, providing new financial services and improving user convenience. It was clearly stated that ensuring an environment that promotes innovation and improves user convenience is one of the important roles expected of the Japan Fair Trade Commission, which is responsible for competition policy.

Fair Trade Commission's criticism of the Zengin System

In 2020, the Japan Fair Trade Commission questioned whether the interbank fees that the Zengin System had set for many years were appropriate, and pointed out that there were problems with the transparency of transactions through the Zengin System and the closed structure of the entire system.

Specific problems were listed as follows:

In reality, the "interbank fees" exceed the administrative processing costs.

The fact that the rates have not changed for over 40 years means that the principle of competition is not working, considering the advancement of information technology and the increase in the number of transactions processed.

According to the "Basic Policy for the Next Zengin System" issued by the National Bank Funds Settlement Network in March 2023, concerns over securing engineers in the medium to long term include the heavy connection burden caused by the use of relay computers (RCs) connecting the Zengin System to each bank, the strong connections and dependencies between components, and low flexibility and scalability.

In addition, the vendor has announced that sales of the mainframe used by the Zengin System will end in 2030 and maintenance will end in 2035, so there are concerns about the issue of securing engineers and rising costs in the medium to long term.

In light of the current challenges, they aim to build a foundation that will allow them to select the optimal infrastructure and connection technology in response to future changes in the technological environment, and as part of this, they have decided to aim for an open system in the next system.

This probably means that by 2035, they will abolish relay computers (RCs) and build an API (application programming interface) gateway.

Although the transition from mainframes to open systems involves certain risks, they stated that with the decision to discontinue sales of the currently used infrastructure, continuing to use it could increase the risks, given that it will become even more difficult to secure the necessary engineers in the future.

Will blockchain and broadly defined stablecoins complement the Zengin-Net?

First of all, I would like to state that the probability of the existing financial system completely disappearing and being replaced by blockchain and stablecoins is extremely low.

This is unlikely to happen at least for the next 10 years. Japan's obsession with cash can be seen in the fact that the situation has remained almost unchanged for many years, despite the fact that the management costs of ATMs are nearly 2 trillion yen per year.

However, as mentioned above, coexistence with existing finance is highly likely to be achieved through the openness of blockchain technology, so I would like to touch on it here as a complementary presence.

In Japan, there are various classifications of stablecoins in the broad sense, such as trust-type coins represented by Progmat, fund transfer-type coins as aimed at by JPYC, and deposit-type digital currencies such as DCJPY, which was announced the other day, and there are several stablecoins with different classifications.

Strictly speaking, Progmat seems to be structured in a way that it can issue stablecoins in other classifications, but based on a past interview with Iolite, I will list it as a trust-type coin here.

Perhaps as a result of the Fair Trade Commission's aforementioned efforts to promote innovation and ensure an environment that improves user convenience, there has been a vigorous movement to issue stablecoins in Japan.

Currently, stablecoins are attracting attention as a complement to the Zengin-Net and existing financial systems, and are particularly likely to be able to compensate for system weaknesses such as low payment fees, fast transaction speeds, and identity verification used by banks.

At present, there are challenges

However, there seem to be two main issues at present:

Few people have the wallets necessary to use stable coins

Taxation method unique to Japan

Few people have the wallets necessary to use stablecoins.

As mentioned in the interview with JPYC's Okabe, it is thought that currently only about 10-15% of Japanese residents own a wallet.

For stablecoins to become part of everyday use, we believe that wallets, which are essential for transactions, need to be owned by everyone, just as smartphones need to become more widespread. It will be essential for them to be included as standard on smartphones released by major mobile carriers, and for smartphone games that require wallets to become a huge hit.

Japan's unique tax system

In addition, even if cryptocurrency-to-cryptocurrency transactions are exempt from taxation under the taxation system that will likely be gradually revised, it is possible that transactions with stablecoins will be subject to taxation.

There are still challenges remaining in providing something that is more convenient and secure than a bank.

Summary

For a very long time, pilot projects have been conducted to effectively utilize blockchain technology in existing financial systems. Perhaps it is fortuitous that the legal reforms regarding stablecoins have occurred at a time when the Zengin Net problem occurred.

With the aforementioned openness, it is very likely that blockchain technology will be used in existing finance, so we hope that it will continue to be used to promote innovation as a complement to existing finance, and that an environment in which it can improve user convenience will be secured.

Image: Shutterstock

Profile

◉Noriaki Yagi While attending university, he worked in the food and beverage industry. From that experience, he launched a restaurant consulting business and a human resources dispatch business in the amusement field, and became its representative. At the same time, he started using social media to establish his own brand. After achieving a total of 10,000 followers on social media, his recognition increased and he launched his own apparel brand. In September 2021, he joined J-CAM Co., Ltd. After working on YouTube and Twitter, he became editor-in-chief in April 2022. In March 2023, he launched "Iolite".