What is cryptocurrency (virtual currency) lending?

Cryptocurrency Lending - Three Key Points

① Lending is a system in which you lend crypto assets and earn interest, and it is an investment method increasingly used by more experienced investors.

Lending crypto assets to exchanges, specialized services, and DeFi services earns interest. It is popular among intermediate and long-term investors because it provides income without being affected by price fluctuations. Stablecoins, in particular, offer high yields and contribute to portfolio stability.

② Risks Beneath High Yields Exist, Including Credit Risk, Liquidity Risk, and Operational Transparency Risk.

Risk factors are diverse, including operator bankruptcy (e.g., Celsius), delayed repayments, opaque management practices, and smart contract vulnerabilities. Domestic exchanges offer high security but low interest rates. Specialized services offer high yields and flexibility, but require risk assessment. DeFi services offer high transparency but require complete self-responsibility and advanced knowledge.

③. Japan is currently developing a regulatory framework, with a focus on transparency, safety, and accountability.

The Financial Services Agency is considering regulating lending as a financial product from 2025 onward. Advertising restrictions, information disclosure requirements, and stricter risk explanations are likely, ushering in an era in which lenders will be discriminated against based on service quality and management structure. For users, a rational strategy would be to diversify across multiple services, comprehensively evaluating interest rates, security, and the reliability of the operating company.

Cryptocurrency lending is a system in which you earn interest by lending your cryptocurrencies, such as Bitcoin (BTC) or Ethereum (ETH), to exchanges or specialized lending services.

Like interest on bank deposits, cryptocurrency lending is unique in that you can earn income simply by depositing your assets, and it is becoming increasingly popular among intermediate cryptocurrency investors.

"This article is for informational purposes only and does not recommend investing in any specific services. Managing cryptocurrencies involves risk. Please make investment decisions at your own risk."

The basic mechanism of lending

Cryptocurrency lending is a system in which users receive interest (lending fees) in exchange for lending their cryptocurrencies. When users deposit their cryptocurrencies with a lending service, those assets are managed for the following purposes:

Sub-lending to exchanges and institutional investors

Investing in funds

Management in DeFi (decentralized finance)

Staking

The service then returns a portion of the profits earned from these operations to users as "interest."

Interest is paid at different times depending on the service, such as daily, weekly, monthly, or quarterly, but they all have one thing in common: "Just by depositing your crypto assets, they automatically increase."

Especially for long-term cryptocurrency holders, this is an effective way to monetize their assets, rather than just watching price movements.

Comparison Table of Major Lending Services

価格変動の影響を受けずに運用できるメリット

The greatest benefit of lending is that, since income is often earned in cryptocurrencies, it can be earned without being directly affected by cryptocurrency price fluctuations.

Cryptocurrency investments are generally focused on capital gains, but lending eliminates the need to sell assets, resulting in the following benefits:

Earn income even during periods of stagnant prices.

Interest can sometimes partially offset losses even during a downturn.

Look for compound interest while holding for the long term.

Investing in stablecoins limits the risk of price fluctuations.

For example, even if BTC falls in the short term, the interest earned from lending will steadily accumulate, contributing to portfolio stability over the long term.

As a "grow without selling" investment method, lending is becoming a core passive income strategy in the cryptocurrency market.

While lending is a convenient investment method, it is important to understand that it also carries certain risks. The main risks are as follows:

● Credit Risk (Operator Risk)

If you deposit your assets with an operator without a cryptocurrency exchange license, there is a risk that your assets will not be returned if the operator goes bankrupt. Past examples of overseas lending operators, such as Celsius and BlockFi, have gone bankrupt, and some services lack sufficient user protection mechanisms.

● Liquidity Risk

Due to sudden market changes or large customer withdrawals, it may take time for the service provider to return funds. Even in the case of domestic exchange-type lending services that are required to manage their assets separately, caution is required, as the liquidation process, identification of user assets, and withdrawal procedures may take time in the event of an operator bankruptcy.

● Operational Transparency Risk

The higher the service's expected yield, the more opaque the investment methods used to generate interest. Furthermore, some services actively use DeFi, which increases the risk of smart contract bugs and vulnerabilities.

●Counterparty Risk

If the counterparty (exchange or company) to which you lend your crypto assets lacks security, your assets may be lost due to hacking or bankruptcy.

As such, it is important to carefully select lending services, keeping in mind that "high yields come with corresponding risks."

Why is lending popular among intermediate and advanced investors?

Cryptocurrency lending is popular with intermediate and advanced investors not just because of its high yields. Its multiple appeals lie in its multiple benefits:

● It's well-suited for long-term asset management.

Intermediate and advanced investors tend to hold cryptocurrencies like BTC and ETH for long periods of time, so lending, which allows them to grow their assets while they hold them, is a logical choice.

● It allows for steady growth of crypto assets without the hassle of buying and selling.

There's no need for market analysis like trading, and interest accumulates automatically once you deposit.

● It allows for high yields with stablecoins.

While bank deposits earn almost zero interest, some stablecoin services offer annual interest rates of around 10%, significantly improving capital efficiency.

● Security measures are evolving and improving safety.

In particular, services using Fireblocks, such as those that use Fireblocks, have become increasingly popular, offering robust security designs that take into account past bankruptcy risks.

● It allows for diversifying portfolio revenue streams.

It allows for a solid revenue base that isn't overly dependent on capital gains.

For these reasons, lending has gained a certain amount of support as a tool for investors who want to step up to intermediate and advanced levels.

There are three types of lending services (exchanges vs. dedicated vs. DEX/DeFi)

Cryptocurrency lending services can be broadly divided into three types: those offered by exchanges, those offered by specialized lending companies, and lending protocols run on smart contracts. Each service has its own advantages and disadvantages, with differences in interest rates, ease of use, and security.

Below, we will compare the features of ① exchange lending (Coincheck, bitbank, etc.), ② specialized lending (Nexo, BitLending, etc.), and ③ DeFi lending (a detailed comparison of Aave and Uniswap) using representative examples.

We will also summarize ④ the points to consider when choosing a service based on user type (beginner to intermediate, long-term holder, high-yield-seeking).

① Characteristics of exchange-type services (lower interest rates but a strong sense of security)

Several major domestic cryptocurrency exchanges offer lending services, and although interest rates are low, their strengths lie in their safety and ease of use. Representative examples include the following:

Coincheck

[PR] *Source: Coincheck (June 10, 2024)

As one of Japan's major exchanges, it supports approximately 36 cryptocurrencies (as of 2025), including major cryptocurrencies such as Bitcoin, Ethereum, and XRP, and allows users to choose their preferred lending period from 14 to 365 days.

Interest rates are set at 1-5% per year depending on the lending period (1% for 14 days, 5% for 365 days). The minimum lending amount is approximately ¥10,000, making it a reasonable starting point, and one of its appealing features is the ability to start with a small amount.

However, cancellations are not possible midway, and once a loan is made, the cryptocurrency will not be returned until the end of the term. Additionally, because the exchange has a limit on borrowing limits, if the application quota is filled, lending may not begin immediately even if you apply.

As one of Japan's leading exchanges, it offers lending for all of the stocks it handles (43 as of 2025), including many altcoins. Interest rates vary depending on the offering period and currency, but in the past, they've typically been set at 1-5% per year, with a maximum annual interest rate of around 5%.

The lending period and minimum amount are determined for each offering, but participation is often possible with a relatively small amount. Mid-term cancellation is generally prohibited, but BitBank makes an exception and allows cancellation in exchange for a 5% principal fee and waives interest.

Therefore, cancellation is possible in an emergency, but be aware of penalties. Popular stocks often fill up immediately after offering begins, and it can take a long time for applications to be approved.

In addition to the above, other domestic exchanges, such as bitFlyer, SBI VC Trade, and BITPOINT, also offer lending services. Each service has different interest rates, supported securities, and conditions, but exchange-related services generally have some common features, such as modest interest rates (up to a few percent per year), no mid-term cancellation (even if possible, large fees apply), and upper limits on lending limits.

Exchanges handle everything from buying and selling, lending, and withdrawals in-house, so it's less hassle and easier for beginners to use, but they also tend to offer lower yields.

② Characteristics of specialized lending services (high yields, but selection is essential)

While specialized cryptocurrency lending services (lending services that do not involve exchanges) offer high interest rates and flexible management, they require a certain level of knowledge and risk tolerance.

Representative services include the internationally-renowned Nexo and the domestically-owned BitLending.

Nexo

Nexo is a major European cryptocurrency lending platform. Founded in 2007 by the European fintech company Credissimo, it has grown into one of the world's largest cryptocurrency lending services thanks to its reliability and scale.

Nexo supports over 100 currencies and instruments, including Bitcoin, Ethereum, stablecoins such as USDT and USDC, as well as its proprietary token, NEXO, and fiat currencies.

Nexo pays a portion of its interest in its proprietary token, the NEXO token. For example, the rate for USDT is 9% (the loyalty program cap is 11% + 2% equivalent in NEXO tokens), and for the major currency, BTC, it is 3% (the loyalty program cap is 3% + 2% equivalent in NEXO tokens).

Interest is automatically compounded and distributed daily, resulting in even higher yields over the long term.

In terms of security, deposited assets are managed in a wallet by BitGo, a major US custody company, and through partnerships with multiple security companies such as Ledger and Bakkt, custodial assets are reportedly insured for a total of $775 million.

The system also boasts a highly reliable management structure, including audits by Armanino LLP and the introduction of "Proof of Reserves," which allows for real-time confirmation of the status of customer assets and liabilities.

Operating company Credissimo has a long history in the financial industry and is well-known for its regulatory compliance and customer protection.

When using the service from Japan, it is important to note that it is provided by an overseas company, Japanese language support is insufficient, and other services provided by the company, such as secured loan services, do not clearly comply with Japanese laws and regulations.

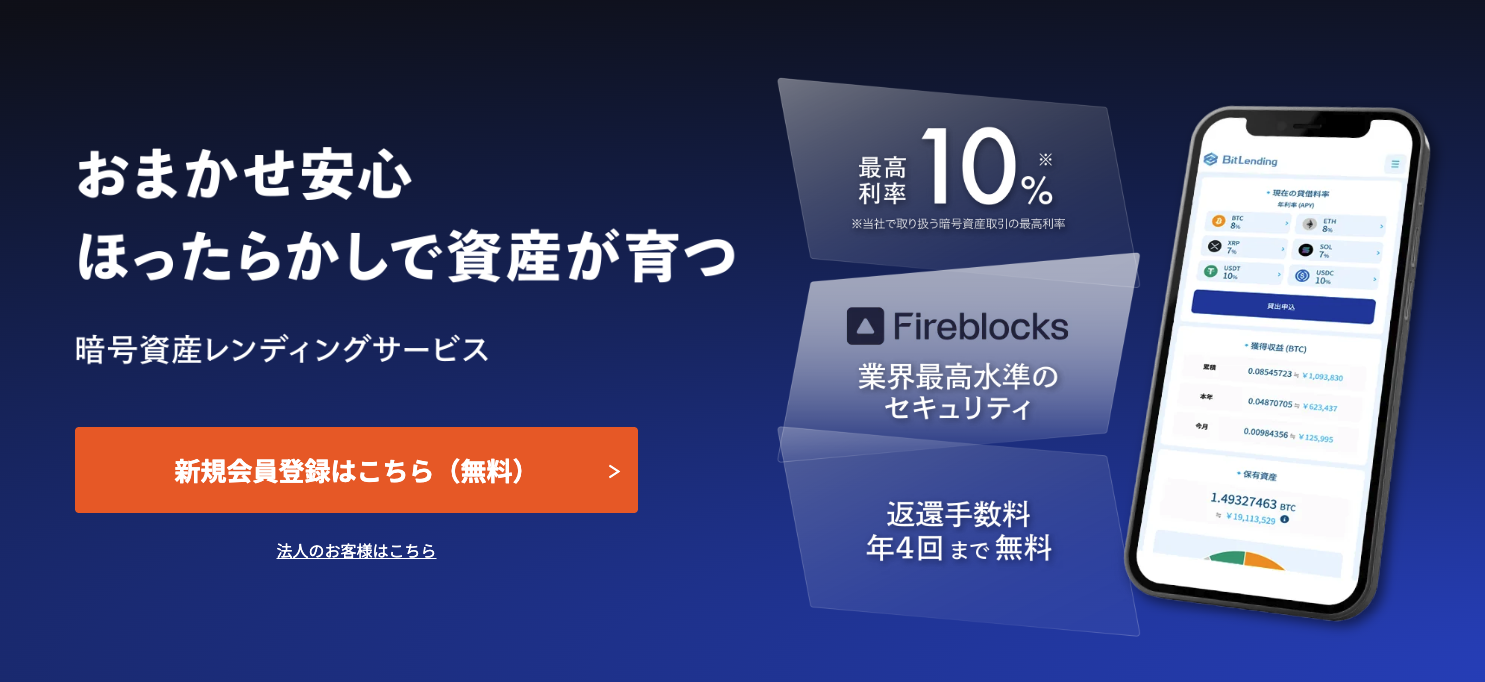

BitLending

J-CAM is a Japanese cryptocurrency lending service operated by the company. It is a relatively new service that began offering services around 2022.

Currently, it supports seven types of cryptocurrencies, including Bitcoin, Ethereum, XRP, Solana, USDT, USDC, and DAI, and boasts "the industry's highest lending fee rates." Interest rates are 8% per year for BTC and ETH, and 10% per year for stablecoins (USDT/USDC/DAI), which are higher than lending rates offered by domestic exchanges.

The minimum lending period is one month, and the service is also notable for its flexibility, allowing withdrawals (cancellations) at any time.

If you wish to cancel your loan midway, you will not be able to withdraw your funds for at least 30 days after the loan begins. After that, your funds will be returned within seven business days of completing the cancellation procedure (no interest will be charged upon cancellation, and a fee may apply in some cases).

In terms of safety, the service diversifies risk by diversifying users' assets across multiple external funds and limiting investment in any one fund to 10% of the total assets.

Furthermore, it appears that measures such as appropriately rotating funds with poor performance are also being taken.

Currently, interest payments and management reports are provided. Account opening and lending can be completed in as little as one day, garnering a certain level of support from long-term holders seeking high yields.

The service's convenience, with accounts opened and lending initiated in as little as one day and refunds made within seven business days of cancellation, appears to make it attractive to domestic users seeking high interest rates.

However, there is a risk that principal will not be reimbursed if management is unsuccessful or the company goes bankrupt.

Therefore, a proper understanding of the fund management system and ability to tolerate risk are prerequisites for use.

③ Characteristics of decentralized (DEX/DeFi) lending services (high yields, but self-defense capabilities are essential)

Lending using decentralized exchanges (DEXs) such as Aave and Uniswap is a non-custodial system in which assets are lent through smart contracts without the involvement of a central administrator.

While offering high interest rates and excellent transparency, it is characterized by the requirement for self-management.

Aave

A leading DeFi lending protocol, Aave allows users to deposit a variety of assets, including USDC, DAI, ETH, and WBTC, as collateral in exchange for interest-bearing aTokens (e.g., aUSDC).

Aave's interest rate fluctuates every block based on supply and demand.

Borrowers can choose between a floating interest rate or a stable interest rate within a certain range. The specific interest rate levels vary depending on market conditions, but historically, interest rates have been around 4-6% per year for stablecoins and 2-4% per year for ETH.

If market demand surges, interest rates can jump into double digits.

Uniswap

While there are no dedicated lending features, the services indirectly earn investment income through liquidity provision (LP).

Users deposit their assets in a currency pair of their choice (e.g., USDC/ETH) and receive a portion of the trading fee revenue.

Annualized returns of around 1-3% are expected, but with highly volatile pairs, there is a risk of "impermanent loss," where market fluctuations reduce asset value beyond the fee income.

These services can be accessed globally with just a wallet, and no KYC or account opening is required, offering a high degree of anonymity and flexibility.

Neither protocol has experienced a major hacking incident, and it can be said that they currently pursue a high level of security.

However, when using emerging decentralized (DEX/DeFi) lending services, users will need to be aware of and deal with all risks, such as hacking, contract bugs, and the risk of liquidation due to sudden price fluctuations.

In addition, there is no custody of assets, and investors are responsible for any loss of assets due to mismanagement of private keys or the use of fraudulent websites.

As a result, while it is possible to aim for high yields, it can be said that this investment method also requires "self-defense capabilities."

Overall, DEX/DeFi lending is structured as "high interest rates but requiring knowledge and management skills" and "high flexibility but no protection," making it an investment method for intermediate to advanced investors.

While the risk of operational failure is theoretically low, it is important to note that investors must make all decisions, store, and handle all transactions themselves.

Overseas, services such as Celsius and BlockFi once existed, but some of these services went bankrupt during the market turmoil of 2022. Therefore, when using a specialized service provider, it is important to carefully assess the operating company's financial soundness and management structure.

As such, while lending provided by exchanges is advantageous in terms of convenience and reliability, specialized services have their own unique appeal, such as high yields and flexible investment plans.

It is best to choose the appropriate service based on your investment style and risk tolerance, taking into account the advantages and disadvantages of each.

Finally, we'll summarize trends and key points for choosing a lending service based on user type. Generally, users are considered to be "beginners to intermediate users," "long-term holders," and "high-yield investors," with each type prioritizing different things.

Beginners to intermediate users: For users unfamiliar with cryptocurrencies or lending in general, we recommend starting with a reliable and easy-to-use exchange-based lending service.

Major domestic lenders such as Coincheck and bitbank offer comprehensive Japanese support, and as long as you have an account with the exchange, you can easily apply for a loan with just one click.

Minimum lending amounts are often set low, starting at around ¥10,000, making it easy to try out a small amount. For beginners, sending assets to an overseas broker immediately due to high interest rates is a high hurdle, and the risks are difficult to predict. Therefore, it is recommended to first earn a few percent of interest on a domestic exchange and understand how it works.

Once you become an intermediate user and gain experience, you can gradually shift some of the funds you feel are lacking from exchange-based lending to specialized services.

Long-term holders: Users who hold on to their Bitcoin and major altcoins for long periods of time are well suited to lending.

This is because, for long-term holders, lending, earning fees, and managing their assets with compound interest is more efficient. For users who are somewhat familiar with cryptocurrency-related services, lending and staking are a good strategy for earning fees and rewards.

Even if you are seeking higher yields, diversifying your assets is a wise strategy if you want to reduce certain risks. For example, allocating half of your assets to exchange lending and the other half to services offered by specialized lending providers and staking can reduce the risk of losing all your assets due to a single risk. By combining multiple reliable services, long-term investors can achieve both asset stability and profitability.

The choice between an exchange, a specialized lending service, or a DeFi-based lending service is truly a trade-off between interest rates and peace of mind. The first step to successful asset management is to choose a service that suits your investment style (safe or aggressive) and goals, while prioritizing the reliability and track record of the operating company. If used appropriately, lending can be a powerful way to increase asset efficiency through long-term holding and income gains. It's important to understand the pros and cons before choosing the lending service that's best for you.

The article is for members only. Please sign up to continue reading.

MAGAZINE

Iolite Vol.21

September 2026 issueReleased on 2026/07/30

Interview Richard Teng, Co-CEO, Binance

Taisuke Isono, Head of Nikko Open Innovation Lab & DeFi Technology Department, SMBC Nikko Securities Inc.

Hiroshi Kamiwaki, Director & Head of Crypto Asset Finance Business, Fintertech Co., Ltd.

PHOTO & INTERVIEW Yusaku Nakano

Feature Story: "Survival Strategies for Crypto Exchanges — The New Order Post-FIEA Transition"

Interview

Tomoyuki Isaka, President & Representative Director, CEO, Coincheck, Inc.

Takaaki Fujiwara, Executive Vice President & Director, Mercury Inc.

[Dialogue Series] The NISHI Talk: Crypto Conversations

"Social Implementation Beyond Merely Holding Bitcoin"

Kasou NISHI × Rintaro Kawai, President & Representative Director, ANAP HOLDINGS Co., Ltd.

Series: Tech and Future Toshinao Sasaki ...and more

MAGAZINE

Iolite Vol.21

September 2026 issueReleased on 2026/07/30

Interview Richard Teng, Co-CEO, Binance

Taisuke Isono, Head of Nikko Open Innovation Lab & DeFi Technology Department, SMBC Nikko Securities Inc.

Hiroshi Kamiwaki, Director & Head of Crypto Asset Finance Business, Fintertech Co., Ltd.

PHOTO & INTERVIEW Yusaku Nakano

Feature Story: "Survival Strategies for Crypto Exchanges — The New Order Post-FIEA Transition"

Interview

Tomoyuki Isaka, President & Representative Director, CEO, Coincheck, Inc.

Takaaki Fujiwara, Executive Vice President & Director, Mercury Inc.

[Dialogue Series] The NISHI Talk: Crypto Conversations

"Social Implementation Beyond Merely Holding Bitcoin"

Kasou NISHI × Rintaro Kawai, President & Representative Director, ANAP HOLDINGS Co., Ltd.

Series: Tech and Future Toshinao Sasaki ...and more

.jpg)

.jpg)